Russia had the chance at the end of the Cold War to build a modern, diversified economy, with the enthusiastic help of the West. That chance has been squandered.

It took two years for crumbling oil prices to bring the Soviet Union to its knees in the mid-1980s, and another two years of stagnation to break the Bolshevik empire altogether.

Russian ex-premier Yegor Gaidar famously dated the moment to September 1985, when Saudi Arabia stopped trying to defend the crude market, cranking up output instead. “The Soviet Union lost $20bn per year, money without which the country simply could not survive,” he wrote.

The Soviet economy had run out of cash for food imports. Unwilling to impose war-time rationing, its leaders sold gold, down to the pre-1917 imperial bars in the vaults. They then had to beg for “political credits” from the West. That made it unthinkable for Moscow to hold down eastern Europe’s captive nations by force, and the Poles, Czechs and Hungarians knew it.

“The collapse of the USSR should serve as a lesson to those who construct policy based on the assumption that oil prices will remain perpetually high. A seemingly stable superpower disintegrated in only a few short years,” he wrote.

Lest we engage in false historicism, it is worth remembering just how strong the USSR still seemed. It knew how to make things. It had an industrial core, with formidable scientists and engineers.

Vladimir Putin’s Russia is a weaker animal in key respects, a remarkable indictment of his 15-year reign. He presides over a rentier economy, addicted to oil, gas and metals, a textbook case of the Dutch Disease.

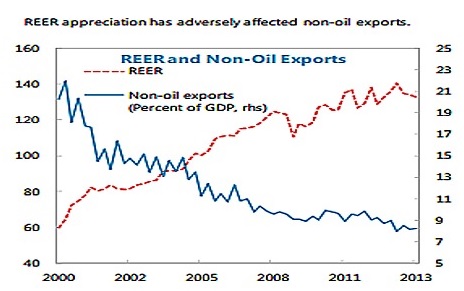

The IMF says the real effective exchange rate (REER) rose 130pc from 2000 to 2013 during the commodity super-cycle, smothering everything else. Non-oil exports fell from 21pc to 8pc of GDP.

“Russia is already in a perfect storm,” said Lubomir Mitov, Moscow chief for the Institute of International Finance. “Rich Russians are converting as many roubles as they can into foreign currencies and storing the money in vaults. There is chronic capital flight of 4pc to 5pc of GDP each year but this is no longer covered by the current account surplus, and now sanctions have caused foreign capital to turn negative, too.”

“The financing gap has reached 3pc of GDP, and they have to repay $150bn in principal to foreign creditors over the next 12 months. It will be very dangerous if reserves fall below $330bn,” he said.

“The benign outcome is a return to the stagnation of the Brezhnev era [Застой in Russian] in the early 1980s, without a financial collapse. The bad outcome could be a lot worse,” he said.

Mr Mitov said Russia is fundamentally crippled. “They have outsourced their brains and lost their technology. The best Russian engineers go to work for Boeing. The Russian railways are run on German technology. It looked as if Russia was strong during the oil boom but it was an illusion and now they are in an even worse position than the Soviet Union,” he said.

The Saudi drama of 1985 has powerful echoes today. We do not know exactly why the Saudis decided to drive down the oil price, though they were clearly frustrated by OPEC cheating, and needed extra revenue themselves.

Ronald Reagan biographer Paul Kengor says the chief motive was to nurture their strategic alliance with Washington, doing a favour for the US at an inflexion point in the Cold War. The former President’s son, Michael Reagan, makes the same claim. “My father got the Saudis to flood the market with cheap oil,” he said. The plans were allegedly hatched by CIA Director William Casey.

By then President Reagan was spending 6.6pc of GDP on defence and building his 15 aircraft carrier battle groups (never quite achieved), inviting ruinous attempts by the USSR to keep up.

The “Reagan Doctrine” twisted the knife further by backing guerrilla insurgencies against Soviet client states: in Afghanistan, Nicaragua and Angola, among others. The Pentagon’s rule of thumb was that it cost Moscow 10 times as much to defend these regimes as it cost Washington to take pot shots. Hawk anti-aircraft missiles were cheap. Soviet MIG 24 helicopters were expensive.

The Saudis were again helpful. They bankrolled the Nicaraguan Contras when House Democrats cut off funding, quietly paying for an off-books operation by US intelligence. The go-between was Prince Bandar bin Sultan, then Saudi ambassador in Washington.

This is the same Prince Bandar – later head of the Saudi secret service – who spent four hours with Mr Putin last year at his dacha outside Moscow. A transcript of their talk was leaked by the Kremlin, in order to embarrass Riyadh. It suggests that the prince offered Russia a deal to carve up global oil and gas markets, but only if it sacrificed Syria’s Assad regime. He purported to speak with the full backing of Washington.

While nothing came of the meeting, it gives a glimpse into the raw geopolitics of oil. It explains why they think the worst in Moscow today as the Saudis cheerfully shrug off a 24pc plunge in Brent crude prices since June. “This is political manipulation, and Saudi Arabia is being manipulated, which could end badly,” said Mikhail Leontyev from Russia’s oil arm, Rosneft.

Events never repeat themselves. The Saudis lack the spare capacity these days to dictate prices with 1980s panache. They have their own pain threshold. Their welfare blitz since the Arab Spring has run to $130bn. The Shia minority in the Eastern Province has a score to settle, and they are sitting on the giant oil fields.

Brent oil has settled at around $85 a barrel. Deutsche Bank said the “break-even price” for the Saudi budget is $99, rising to $100 for Russia and Oman, $126 for Nigeria, $136 for Bahrain and $162 for Venezuela. There is a widely-held view that the Saudis are bluffing in order to force the rest of OPEC to agree to output cuts. If so, we will find out in November.

What is clear is that the Saudis can withstand two or even three years at the current price by dipping into their $745bn foreign exchange reserves. This would have the added bonus (for them) of chilling fresh shale ventures, and perhaps killing some deep water forays in the Atlantic.

Whatever the Saudi motive, Russia is already reeling. The central bank governor Elvira Nabiulina told the Duma last week that plans are afoot to cope with a protracted slide in oil prices to $60. “We are working on a stress scenario, an emergency scenario so to speak,” she said.

Moody’s said the central bank has burned through $60bn of foreign reserves since the end of last year propping up companies starved of dollar liquidity. The total has dropped to $396bn on its estimates (leaving aside the Reserve Fund) and is becoming a sovereign credit risk.

This time Russia is not facing Reaganesque rearmament, but it is facing nuclear-tipped sanctions, more destructive than many realise in a globalised banking system. It is not a stretch to say that American regulatory power has never been so far-reaching, or imperial. The result is that Russian banks, companies and state bodies are shut out of the global capital markets, unable to roll over $720bn of external debt.

Russia’s reserves of cheap crude in West Siberian fields are declining, yet the Western know-how and vast investment needed to crack new regions have been blocked. Exxon Mobil has been ordered to suspend a joint venture in the Arctic. Fracking in the Bazhenov Basin is not viable without the latest 3D seismic imaging and computer technology from the US. China cannot plug the gap.

Andrey Kuzyaev, head of Lukoil Overseas, said it costs $3.5m to drill a 1.5 km horizontal well-bore in the US, and $15m or even $20m to drill the same length in Russia. “We’re lagging by 10 years. Our traditional reserves are being exhausted. This is the reality for our country,” he said.

Lukoil warns that Russia could ultimately lose a quarter of its oil output if the sanctions drag for another two or three years.

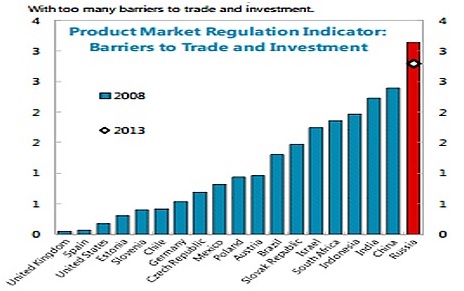

The IMF’s latest “Article IV” report on Russia is an acid verdict on the Putin era. Product market barriers are the worst of any large country in the world. The economy is a tangle of bottlenecks. Russia’s development model has “reached its limits”.

For details, try the World Economic Forum’s index of competitiveness. Russia ranks 136 for road quality, 133 for property rights, 126 for the ability of firms to absorb technology, 124 for availability of the latest technology, 120 for the burden of government regulation, 119 for judicial independence, 113 for the quality of management schools, 107 for prevalence of HIV, 105 for product sophistication, 101 for life expectancy and 56 for quality of maths and science education. This is the profile of decline.

Russia had a window of opportunity at the end of the Cold War to build a modern, diversified economy, with the enthusiastic help of the West, before the ageing crisis hit and the workforce began shrink by 1m a year. This chance has been squandered. Mr Putin’s rash decision to pick a fight with the democratic world has made matters infinitely worse. Cheap oil could prove to be the death knout.

With thanks to Ambrose Evans-Pritchard for giving his permission for us to reproduce his excellent article. It can be viewed on The Telegraph website HERE.